Cement plants are responsible for approx. 6% of CO2 emissions from large Polish industry and power sector. They emit more CO2 than one and a half Turów power plant. The challenges related to decarbonization of this sector go beyond providing clean electricity or heat.

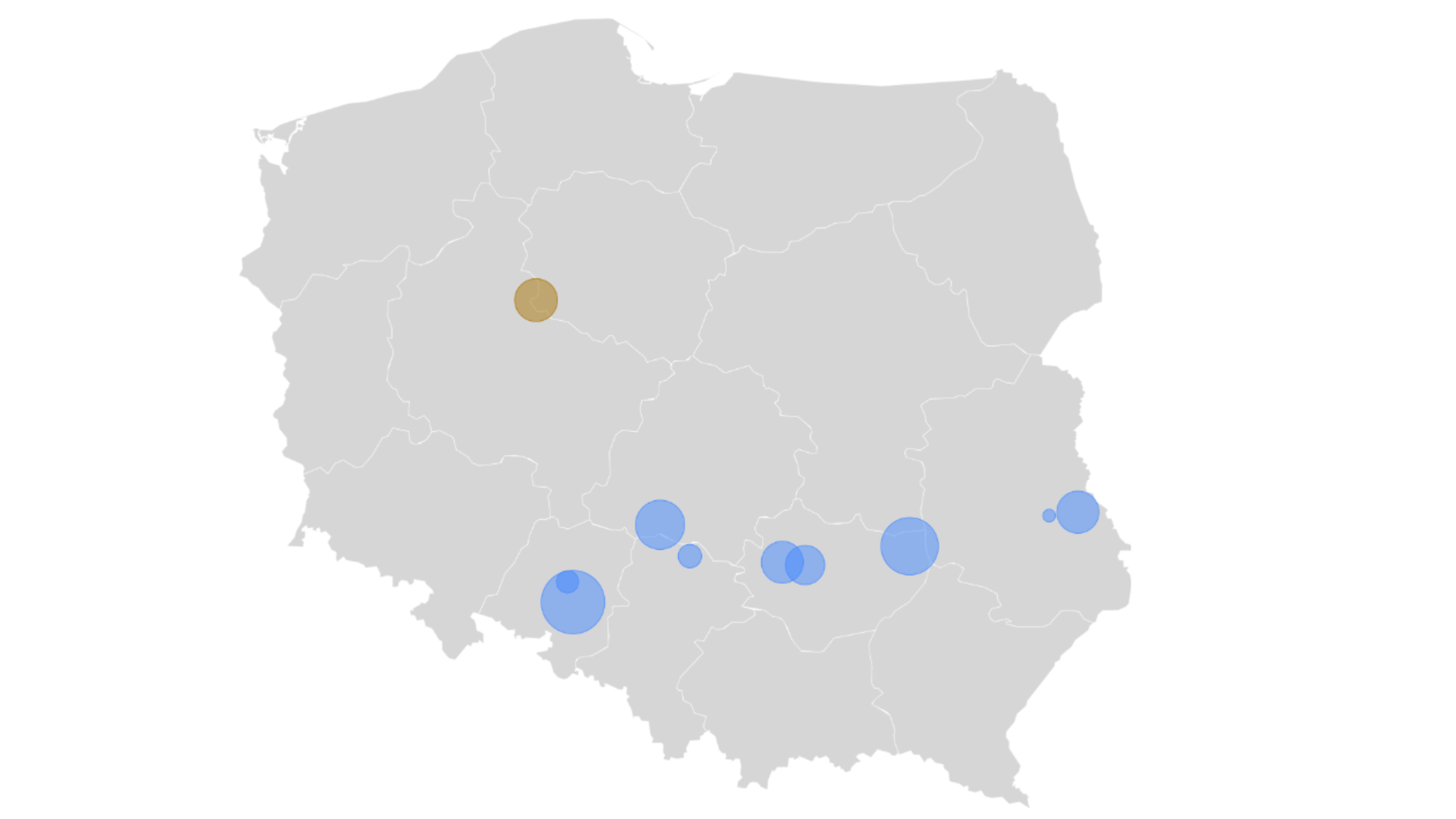

The “Cement Belt” runs from the southern Lublin region, through the Świętokrzyskie, Śląskie and Opolskie Voivodeships. There are limestone rocks in this area, and lime is the basic component of clinker used to produce cement.

Database of CO2 emmissions from EEI in Poland 2010-2020 prepared by the Instrat Foundation on the basis of E-PRTR and KOBIZE (National Center for Emissions Management), which covers larger industrial plants, indicates that between 2015 and 2020 there were 9 large cement production plants in the Cement Belt, and only one was located in another part of the country.

In the period from 2015 to 2020, these cement plants in the Lubelskie, Świętokrzyskie, Łódzkie, Opolskie and Śląskie Voivodeships emitted a total of over 60 million tons of CO2 (on average over 10 million tons per year), i.e. approx. 6% of emissions from the entire Polish industry included in E-PRTR, including power sector.

However, the E-PRTR emissions do not include all emissions from the economy, but only those from the largest companies. The cement plants from the Cement Belt alone in this period amounted to approx. 3% of the entire Polish emissions, i.e. including emissions not only from industry, but also from e.g. homes or individual transport.

The fact that the cement sector is concentrated in only 5 voivodeships means that its situation has a significant impact on the situation of the entire southern part of the country. In the Lubelskie Voivodeship, in this period, cement plants accounted for more than a quarter (27%) of all emissions from the industry covered by the E-PRTR database. And importantly, this list also includes power plants. In the Świętokrzyskie and Opolskie Voivodeships, the importance of cement plants was slightly smaller as they accounted for 19% of emissions.

Decarbonization of cement production could significantly translate into reduction of emissions of voivodeships located in the Cement Belt. The implementation of appropriate investment projects would help these regions to implement the climate policy. Such ambitions already exist in the Eastern Greater Poland with the aim of achieving climate neutrality by 2040 (read Instrat report about contribution of emitting companies to the implementation of the region’s climate policy).

The problem is that reduction of emissions in this sector has its own difficult specificity.

Clean energy is not enough

Emissions related to heat generation, transport or operation of machines may be eliminated through direct electrification (e.g. green energy PPAs) or hydrogen from zero-emission energy sources. For years, cement plants have improved their balances of emissions by using the refuse derived fuel (RDF). However, the cement production has such specificity that emissions related specifically to heat generation or transport account for less than half of the total cement plant emissions. Most emissions are related to a technological process which is of key importance to cement production – producing clinker. Data on the cement sector in Australia show that such process emissions are approx. 55% of total emissions from the cement plant, data for the global average indicate approx. 52%. In other words: limestone rocks cannot be processed into cement today without emitting huge amounts of carbon dioxide.

Due to the fact that decarbonization of electricity and heat supplied to plants may reduce emissions from this sector by only approx. 50%, two main scenarios of achieving climate neutrality are considered in the cement sector. The first one plans to capture the carbon dioxide emitted in the technological process and store it underground or use it to produce other products, e.g. plastics. The second direction is to move away from the most popular Portland cement to other materials with similar properties, namely geopolymers.

The first difficulty in capturing and storing carbon dioxide emitted by cement plants is costs. Investment projects that could make this possible require a lot of expenditures and the regulatory environment has so far attracted little investment. There is also no full support from those financing such projects. Analyses carried out on the basis of examples from the United Kingdom show that such modernization doubled investment and operating expenses in 2015 in the economic context of the United Kingdom. McKinsey & Company’s 2020 analysis indicates that the cost of avoiding emissions of one ton of CO2 when using capture and storage technology could vary between $50 and $200 depending on the specific location, access to infrastructure and economic environment. The authors of the report

conclude that decarbonization of cement production is not yet financially viable. However, this conclusion may be obsolete given rising emission prices, other regulatory instruments and technological investments.

Nevertheless, perhaps due to the expected tightening of the emission policy in Poland and in the European Union, works on the use of carbon capture and storage technologies in cement plants in Poland are in progress. They are carried out, among others, by the Górażdże cement plant and Lafarge Polska (in the Kujawy cement plant). The latter facility implements, with the support of the European Commission (Innovation Fund), a project for carbon capture, liquefaction and transport to the Port of Gdańsk from where the liquefied gas is to get to the depleted offshore oil and gas fields. Whereas, Górażdże (Opolskie Voivodeship) implements the carbon capture program in cooperation with international partners and with the support of the EU’s Horizon 2020 program under the “ACCSESS” project.

The use of offshore mining fields is a response to the second problem related to the implementation of the carbon capture technology, which is the need for access to suitable geological reservoirs or deposits where the captured carbon dioxide could be stored. Depending on the storage method used, either appropriate geological structures or rock caverns are best suited for this purpose, but they are existing formations or formations produced during other projects. However, they may not necessarily be found in the vicinity of present cement plants, and they are difficult to dig. In turn, the use of captured CO2 for other industrial activities requires the construction of new plants and finding a market for their products. One example of such actions is the integration of the Turów power plant with the nearby tomato plantation – heat and carbon dioxide from the power plant make production in greenhouses more efficient. However, this is an isolated example. Whereas, transport of gas to remote storage sites means additional costs.

In addition to carbon capture from cement production, efforts can be made to reduce emissions by switching plants from Portland cement, which inevitably requires high emissions, to cement substitutes. Barriers related to such move are, on one hand, higher production costs and, on the other hand, the fact that the cement industry is currently located in Poland in specific places with appropriate limestone formations. Therefore, switching production to geopolymers may mean, firstly, the need to change the location of the plant or to import raw materials, secondly – it requires the construction of new plants, as the technological process of production of geopolymers is completely different than in the case of Portland cement. The geography of the industrialization of the 19th and 20th centuries is different from the needs of decades to come, said analysts of the Brussels’ Bruegel think tank. And here is another example.

Increasing costs of emission allowances and pressure to reduce them force manufacturers to adapt. Survival of plants and maintaining their competitiveness are important not only from the point of view of owners or shareholders, but also due to the social and economic importance of the cement plants for the entire Cement Belt and for the entire Poland. At the same time, the European carbon tariffs (CBAM) will be necessary to ensure that emissions from the declining cement sector in Europe are not simply transferred to other countries.

As in the case of Upper Silesia and Western Lesser Poland, where hard coal mining was concentrated, if it is necessary to suddenly decarbonize the cement sector, the Cement Belt may experience painful shock.

Cement foundations of the economy

The data provided by the Statistics Poland (GUS) do not allow for a thorough review of the cement sector at the voivodeship level. We have to rely on the overarching category of production of products from other non-metallic mineral resources. This means that the values reported further on cement itself are certainly lower than for the whole sector.

We know that the entire sector of production of products from other non-metallic mineral resources accounts for more than 30% of the total sold value of the industry in the Świętokrzyskie Voivodeship. Much less, but still 15%, is in the Opolskie Voivodeship, and 6 and 7% in the Łódzkie and Śląskie Voivodeships, respectively.

This means that the problems of the cement sector would be hardest at the heart of the Cement Belt, i.e. the Świętokrzyskie Voivodeship.

However, the economic blow would probably be higher than the blow related to direct employment in cement plants. According to 2017 estimates of the Polish Cement Association, cement plants are responsible for creating 4 thousand jobs directly and indirectly for approx. 25 thousand

But these figures cover only part of the entire long supply chain which depends on cement plants, such as construction sector, concrete works, machinery manufacturers or production support.

The discussion on decarbonization of cement production also includes material substitution – activities such as reducing the use of cement in favor of, among others, construction of wooden buildings. However, such activities, even if successful, will not contribute to enabling the sector and plants to continue operations, but to reducing demand for their products. Therefore, this will not save jobs and economic benefits from the operations of a large sector of the Polish economy.

Bibliography:

1. Limestone rocks, zpe.gov.pl, available online at: https://zpe.gov.pl/a/skaly-wapienne/DMgiyBEHJ (January 20, 2023).

2. The database prepared by Instrat is based on the E-PRTR database, available on-line at: https://www.eea.europa.eu/data-and-maps/data/industrial-reporting-under-the-industrial-6, as of November 2022. The E-PRTR database includes plants above certain capacity thresholds indicated in the supplement to Regulation (EC) No 166/2006 of the European Parliament and of the Council of 18 January 2006, available online at: https://www.gios.gov.pl/images/dokumenty/prtr/rozporzadzenie_166_2006.pdf. This means that the database does not cover smaller plants in individual sectors. However, the missing data were supplemented on the basis of KOBIZE data. Note! The Instrat database includes only energy intensive sectors, so calculations taking into account other sectors (calculation of values for the entire industry or for the entire power sector) are made on the basis of the unmodified E-PRTR database.

3. Sectors other than energy intensive industries have not been prepared in the Instrat database, their data are from an unmodified E-PRTR database. This means that the denominator in this division is probably understated, so the share of cement plants may be lower.

4. Polish emission data according to OWiD. H. Ritchie, M. Roser, P. Rosado (2020) – “CO₂ and Greenhouse Gas Emissions.” Available online at: https://ourworldindata.org/co2/country/poland (access on January 17, 2023).

5. Calculations performed for the cement sector in Australia. Beyond Zero Emissions, Rethinking Cement, available online at: https://bze.org.au/research_release/rethinking-cement/ (January 17, 2023). It is uncertain whether this value is the same in Polish cement plants, but due to standardization of the technological process and characteristics of Portland cement the value is probably similar.

6. McKinsey, Laying the foundation for zero-carbon cement, 2020, available online at: https://www.mckinsey.com/industries/chemicals/our-insights/laying-the-foundation-for-zero-carbon-cement (January 25, 2023).

7. To find out more about various methods of underground carbon dioxide storage, read K. Górska, Geological CO2 storage, available online at: https://naukaoklimacie.pl/aktualnosci/geologiczne-magazynowanie-co2/ (January 17, 2023) and Geological methods of CO2 bonding, available online at: https://naukaoklimacie.pl/aktualnosci/geologiczne-metody-wiazania-co2-2/ (January 17, 2023).

8. The data are from the report published in 2015. At that time, the cost of emission certificates was significantly lower than at present. On the other hand, the cost of implementing the technology could have decreased compared to seven years ago. Cf Department of Energy and Climate Change, Industrial Decarbonisation And Energy Efficiency Roadmaps To 2050 – Cement, 2015, available online at: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/416674/Cement_Report.pdf (January 20, 2023).

9. McKinsey, op. cit., Calculations include CO2 emission prices.

10. Polish Cement Association, Cement sector, flywheel of the economy. What challenges does it face?, available online at: https://www.polskicement.pl/aktualnosci/branza-cementowa-kolem-zamachowym-gospodarki-jakie-wyzwania-przed-nia-stoja/ (January 17, 2023).

11. Ibidem.

12. Gorazdze.pl, Górażdże Cement Plant is developing a pilot project for carbon capture in Eastern Europe, available online at: https://www.gorazdze.pl/pl/cementownia-gorazdze-rozwija-pilotazowy-projekt-wychwytywania-dwutlenku-wegla-w-europie-wschodniej (January 25, 2023).

13. Cf K. Górska, Geological…, op. cit.,

14. Tomatoes were a good choice, “Gazeta Wrocławska”, June 9, 2016, available online at: https://gazetawroclawska.pl/pomidory-byly-strzalem-w-dziesiatke/ar/10163074 (January 17, 2023).

15. G. Zachmann, B. McWilliams, A new economic geography of decarbonisation?, Bruegel.org, available online at: https://www.bruegel.org/blog-post/new-economic-geography-decarbonisation (January 25, 2023).

16. P. Piestrzyński, Good forecasts for the cement sector, Cement Report, available online at: http://www.nbi.com.pl/assets/NBI-pdf/2017/5_74_2017/Pdf/19_SPC.pdf (January 18, 2023).